On January 6th, the SC Public Interest Foundation wrote a an article outlining events that highlighted problems with the state’s finance and accounting practices from 2012 to the present. These included accusations of lost funds, leading to the resignation of the state’s Comptroller General and a Senate trial of the state’s Treasurer. As reported in the article, the investigation was plagued by accusations and allegations, which undermined citizens’ trust in their state government’s financial transparency.

The article concluded, “The silver lining is the General Assembly engaged The AlixPartners, an internationally recognized financial accounting firm, to review all aspects of the state’s financial reporting procedures and to provide a report with recommendations. Their report, released on January 15, 2025, identified twenty-five recommendations: twenty of which are specific to the Comptroller General’s Office, one recommendation specific to the State Treasurer’s Office, and three combined to the State Auditor, Treasurer, and Comptroller General. The General Assembly then directed the Governor and the agencies to form the Governor’s Task Force to implement all 25 recommendations.

The legislative bill that outlines the implementation of the recommendations (S.253) indicates that all recommendations not requiring statutory changes should be fully implemented no later than March 7, 2026.”

Deadline Approaching

Vast financial reform is not easy to accomplish. The completed and ongoing work from the State Auditor, Comptroller General, and Treasurer offices is applauded. With the State Treasurer’s office completing its recommendations and the CGO and State Auditor still having some of their recommendations yet to be completed, it is important to remind them that they have until March 7, 2026, to complete the recommendations. Once these recommendations are fulfilled, the State Government will have come a long way towards rebuilding the people’s trust in them handling the State’s funds.

Overview of AlixPartners Recommendations Implementation

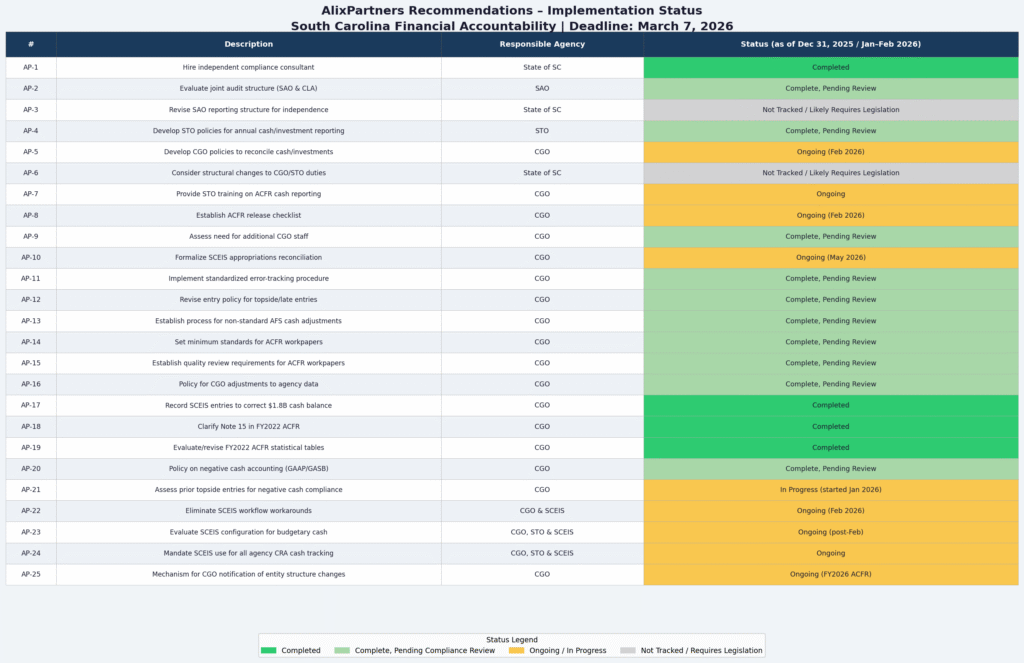

The AlixPartners Forensic Accounting Review Final Report (January 15, 2025) outlined 25 recommendations to address systemic issues in South Carolina’s financial reporting processes, particularly those contributing to the $3.53 billion cumulative overstatement in General Fund cash and equity from FY2012–2021 due to a double accounting error and an appropriations mapping error in the Annual Comprehensive Financial Report (ACFR). These stemmed from issues in the Comptroller General’s Office (CGO), State Treasurer’s Office (STO), and State Auditor’s Office (SAO), including improper topside entries, lack of reconciliations, and inadequate documentation.

Senate Bill S.253 (ratified 2025) established the Governor’s Task Force on Financial Reporting Improvements, requiring implementation of all non-statutory recommendations by March 7, 2026. Progress is monitored monthly by Forvis Mazars (the independent compliance consultant hired under Recommendation 1) and reported at public task force meetings. The latest available minutes are from the February 5, 2026, meeting (covering status as of December 31, 2025, with January 2026 updates noted). No February meeting minutes were found, and the next is likely in March.

Current Progress Summary (as of latest data):

- Completed: 3 recommendations (AP-17, 18, 19).

- Completed, Pending Compliance Review: 9 recommendations (AP-2, 4, 9, 11, 12, 13, 14, 15, 16). These are effectively implemented but await final verification by Forvis Mazars.

- Ongoing/In Progress: 10 recommendations (AP-5, 7, 8, 10, 20, 21, 22, 23, 24, 25), with projected completions from February–May 2026 or later (e.g., FY2026 ACFR cycle).

- Not Explicitly Tracked in Minutes: 3 recommendations (AP-1, 3, 6). AP-1 (hiring the compliance monitor) is complete, as Forvis Mazars was engaged. AP-3 and AP-6 involve structural/legislative changes and may extend beyond the deadline.

This totals 12 fully or nearly completed (completed + pending review), with 13 remaining (ongoing + untracked). Given the proximity to the March 7 deadline (today is February 14, 2026), several ongoing items (e.g., AP-20, 21, 22) are slated for February completion and may be finalized soon. The FY2025 ACFR was released recently without disclosures of restatements, mapping errors, or topside adjustment issues—indicating material progress in resolving the core problems, though full verification awaits task force reports.

Special Attention to Recommendations 20–23 (CGO-Focused on Budget/ACFR Handling): These target the CGO’s topside accounting entries and budget processes, which enabled the original mapping error by allowing manual adjustments via spreadsheets outside the SCEIS system.

- AP-20 (Negative Cash Policy): Ongoing as of December 2025; verbiage agreed and marked “Complete, Pending Compliance Review” in January 2026. Likely resolved by deadline.

- AP-21 (Assess Prior Topside Entries): Not started as of December 2025; initiated in January 2026. Critical for ACFR accuracy; delay risks ongoing miscalculations if not completed soon.

- AP-22 (Eliminate SCEIS Workarounds): Business requirements document submitted; user acceptance testing expected in February 2026. On track for the deadline.

- AP-23 (Evaluate SCEIS Configuration): Ongoing; draft best-practices summary from peer-state reviews (e.g., PA, SD, TN, MA, AR) under CGO review as of December 2025. Expected completion post-February, but may spill over.

If these are not fully implemented by March 7, the FY2026 ACFR (due later in 2026) could face complications from the unreconciled recommendations. Below is a chart to view the ongoing status of the recommendations.